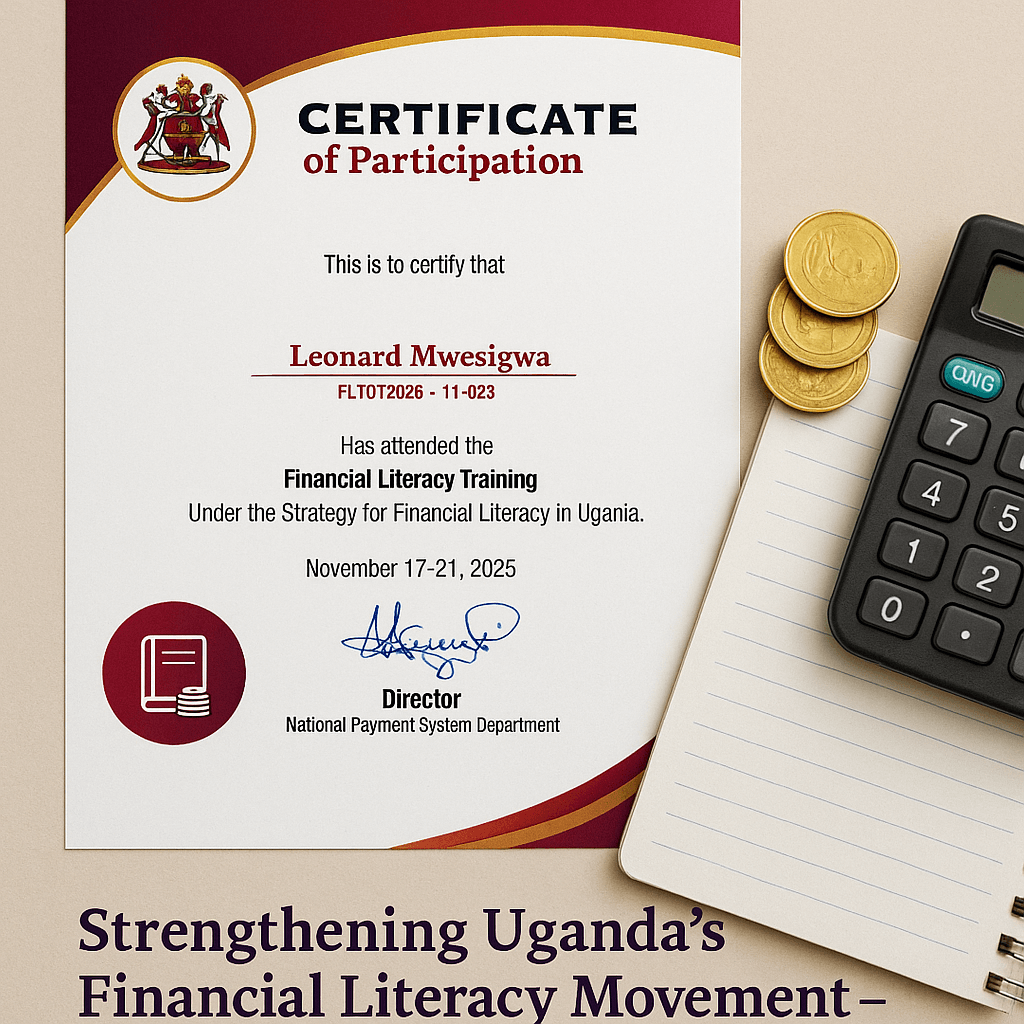

Last week, I was privileged to be part of the team that underwent the Financial Literacy Training of Trainers organized by the Bank of Uganda (BoU). We were entrepreneurs, CEOs, senior managers, accountants—people you would naturally expect to be experts at money management. After all, they run companies, right?

But here’s what shocked me.

While most participants expertly applied financial discipline at the company level, many quietly admitted that they struggle to apply the same discipline to themselves as individuals. If they treated themselves as entities, they would have personal budgets, track expenses, set financial goals, save regularly, manage credit carefully—and ultimately enjoy more predictable and prosperous lives.

That realization set the tone for the entire training.

A senior official from the Bank of Uganda who officially opened the programme emphasized that financial literacy is the first pillar in the Central Bank’s Strategy for Promoting Financial Inclusion. The other pillars are:

- Financial Consumer Protection

- Financial Innovations such as mobile money and agent banking

- Financial Services Data and Measurement

The overall goal of Financial Literacy? – To equip Ugandans with the knowledge, skills, and confidence to manage their finances effectively—to make sound financial decisions, reduce debt, increase savings, protect themselves from exploitation, and ultimately achieve financial well-being.

A Room Full of Experts, Yet So Much to Learn

It was an amazing experience. You know meeting Founders, CEOs, and Senior managers—people you’d assume had mastered the art of money simply because their organizations survive on financial decisions — yet, the surprise was humbling. Many confessed that while they managed corporate finances well, they struggled to apply those same principles to their personal lives.

That’s when the brilliant yet humble Ms. Justine Namata, Manager Financial Literacy at the Central Bank, said something that shifted the room’s energy:

“This training will enrich you at three levels—individual, family, and community.”

Every eye lit up. And indeed, every session delivered on that promise.

Each morning, Mr. Hashim Kirungi from the Financial Literacy Unit at BoU, whose passion for financial literacy was evident in every session reminded us to learn, unlearn, and relearn. And he was right. Much of what we learned was simple, almost obvious—but we weren’t doing it.

As Darren Hardy said:

“What’s simple to do is also simple not to do.”

And that is where most Ugandans, no matter their level of education or income, fall off track.

A GPS for Personal Financial Management

In my earlier article, From Excuses to Execution: Start Your Side Hustle With a GPS, I introduced the concept of a GPS:

G — Goal: Where do you want to go?

P — Plan: What route will get you there?

S — System: What daily actions will keep you on track?

Personal financial management also begins with a GPS!!

You cannot manage what you cannot see. And you cannot move forward if you don’t know where you’re starting from.

This module reminded me of my friend Lucius—a brilliant professional who earns “a lot of money by Ugandan standards”—yet at the end of every month, has no trace of where it went. Lucius is not alone. Many Ugandans, regardless of income, are in the same boat. They work, they earn, they spend, and somehow the money disappears with the speed of data loaded on a teenager’s smart phone.

So today, let me teach Lucius—and many like him—the foundational lessons of Personal Financial Management.

Understanding Personal Financial Management

Personal Financial Management is simply planning and keeping track of your income and expenses using a budget.

Not complicated formulas. Not advanced accounting software. Just understanding what comes in, what goes out, and what stays.

Simple, yes—but remember Darren Hardy:

“What’s simple to do is also simple not to do.”

The magic is not in the complexity.

The magic is in the consistency.

Let’s break it down.

1. Start With Your Financial Goals (Your GPS ‘G’)

A financial goal is simply something you want to achieve that requires money. Not vibes. Not hope. Money.

It could be building an emergency fund to protect yourself from shocks, paying off debt so you can breathe again, buying land, constructing a home, funding your education or your child’s, starting a business, or simply creating a future where money is a tool—not a source of stress.

Reaching financial goals requires four things: knowing how much you earn and spend, understanding the real cost of your goals, deciding how much you will save, invest, or allocate toward debt, and finally determining how long each goal will realistically take.

Lucius, your first assignment is simple:

Write down your top three financial goals for the next 12 months.

If you can’t write them down, you cannot achieve them.

2. Understand Your Income and Expenses

If there’s one question Lucius hates, it’s this one:

“My brother, how much do you spend in a month?”

He always scratches his head, laughs it off, and says, “Eh, me I just survive.”

But survival is not a financial plan.

You must know your income streams—salary, allowances, side hustles, rental income, business profits—and you must know your expenses—food, rent, school fees, transport, data, airtime, supporting relatives, utilities, medical needs, debt payments, weekend outings, and those spontaneous things that seem small but accumulate very fast.

Once you start writing things down, you will be shocked at where your money actually goes. For many Ugandans, the truth is simple:

We don’t have a money problem—we have a tracking problem.

3. Needs vs Wants: Your First Real Test

Personal financial management boils down to distinguishing between needs and wants.

A need keeps you alive, healthy, or able to work—food, transport, shelter, medication, and basic utilities.

A want… well, a want is that thing you “must” buy simply because you feel like it.

Ugandans lose a lot of money to wants disguised as needs. The Thursday-to-Sunday escapades, the shoes you didn’t need but bought because the salesperson called you “Boss,” the unplanned mobile money transfers, the snacks you don’t remember buying but apparently paid for ten times that week.

Lucius once told me, “I don’t know where my money goes.”

I replied, “Your money knows where it went. You are the one who doesn’t know.”

4. Create a Budget (Your GPS ‘P’)

A budget is simply a money plan—a clear outline of what you intend to do with your income. It helps you decide before the month begins how your money will work for you.

Without a budget, your money will work for everyone else—family members, friends, boda boda riders, impulse purchases, social events—except you.

Budgeting is not about restricting yourself; it is about directing yourself.

It is your monthly financial map.

And the best part? It does not need to be perfect. It just needs to exist—and be updated.

5. Track Your Expenses (Your GPS ‘S’)

A budget without tracking is like a gym membership without actually going to the gym. It gives you hope, but no results.

Tracking expenses is where transformation happens. You become aware. You gain clarity. You see patterns. You stop lying to yourself. And you begin to take control.

At first, it may feel tedious—but after two weeks, you will start to enjoy the honesty that comes with it. Even Lucius, who once swore he couldn’t track his spending, confessed that after writing things down for one month, he finally understood why he was always broke by the 20th.

Awareness is power.

6. Reduce Unnecessary Spending

Once you start tracking, something magical happens—you begin seeing opportunities to save money.

You realize how much you spend on things you could reduce or eliminate. You become more intentional. You start planning ahead instead of reacting.

Lucius once told me, “I just don’t know how to save.”

I told him, “You do know how to save. You just spend your savings before they become savings.”

Reducing spending creates room for saving.

7. Keep Proper Financial Records

If you were to disappear for six months, could someone step into your life and understand your finances from your records?

For many Ugandans, the answer is no.

Good financial record-keeping prevents surprises, protects you from exploitation, helps with planning, and gives clarity. It is a discipline every financially empowered adult must develop.

Financial Literacy Is for Everyone

Whether you earn UGX 200,000 or UGX 20 million a month, personal financial management applies to you. Everyone needs to know how to create and follow a budget, distinguish needs from wants, save for emergencies, borrow responsibly, make informed choices about financial products, and plan ahead for old age.

Unfortunately, many Ugandans lack the knowledge, skills, and confidence to do these things consistently. That is why many people who can afford to save do not save, why debt levels remain high, and why many are not benefiting from financial services that could transform their lives.

This is the motivation behind Uganda’s national push for financial literacy.

Conclusion: From the Classroom to Lucius’s Wallet—and Yours

When the training ended, expectations had been exceeded. We walked in as experienced professionals. We walked out with a renewed understanding of ourselves.

Financial literacy is not about having a lot of money—it is about having control over the money you have.

Lucius’s story is the story of many Ugandans.

They earn. They spend. They hope. But they lack a system.

And without a system, money slips through the fingers.

Your journey starts today—with a goal, a budget, a tracking habit, and the discipline to separate needs from wants.

This is the first article in a new series.

In the coming weeks, I will explore:

- Savings

- Loan management

- Investment

- Planning for retirement

- Insurance

- Understanding financial service providers

- Digital financial literacy

If we want a financially empowered Uganda, the transformation must begin in our homes and in our personal lives—not just in our workplaces.

Let’s walk this journey together.

Until next time,

Believe. Build. Be Bold.

— Dr. Mwesi Leo Career & Business | Productivity Systems | Financial Freedom

Career & Business | Productivity Systems | Financial Freedom

Comment |

Comment |  Share |

Share |  Like |

Like |  Subscribe

Subscribe

You May Also Like

Leave Your Comment:

Leave Your Comment:

{kind=link}

Comments (7)

Naijuka Arthens,

11 November, 2025We Humbly appreciate you Dr. Thanks for inspiring us GBU

drmwesileo,

11 November, 2025Thank you for the feedback! I appreciate it. Let’s take it action now!

Naijuka Arthens,

11 November, 2025Thanks for inspiring us GBU

Thomas Epeet,

11 November, 2025Much appreciated. Very practical and good for the nation

drmwesileo,

11 November, 2025Wow! Thank you so much Engineer for appreciating the efforts. Indeed it is good for the nation. If we can manage our finances well, ultimately the country’s finances shall get in order.

Why Many People Struggle to Save Money—and Simple Steps to Start Saving Today – Dr. Mwesigwa Leonard,

12 December, 2025[…] (If you missed the Article, catch up here: Personal Financial Management: A Practical Guide to Budgeting, Tracking Expenses, and Setting Goals). […]

Why Your Definition of Success Is Probably Wrong (And What to Pursue,

06 June, 2026[…] Read: Personal Financial Management: A Practical Guide to Budgeting, Tracking Expenses, and Setting Goals. […]